Florida’s Property Insurance Crisis Will Likely Get Worse After Hurricane Ian

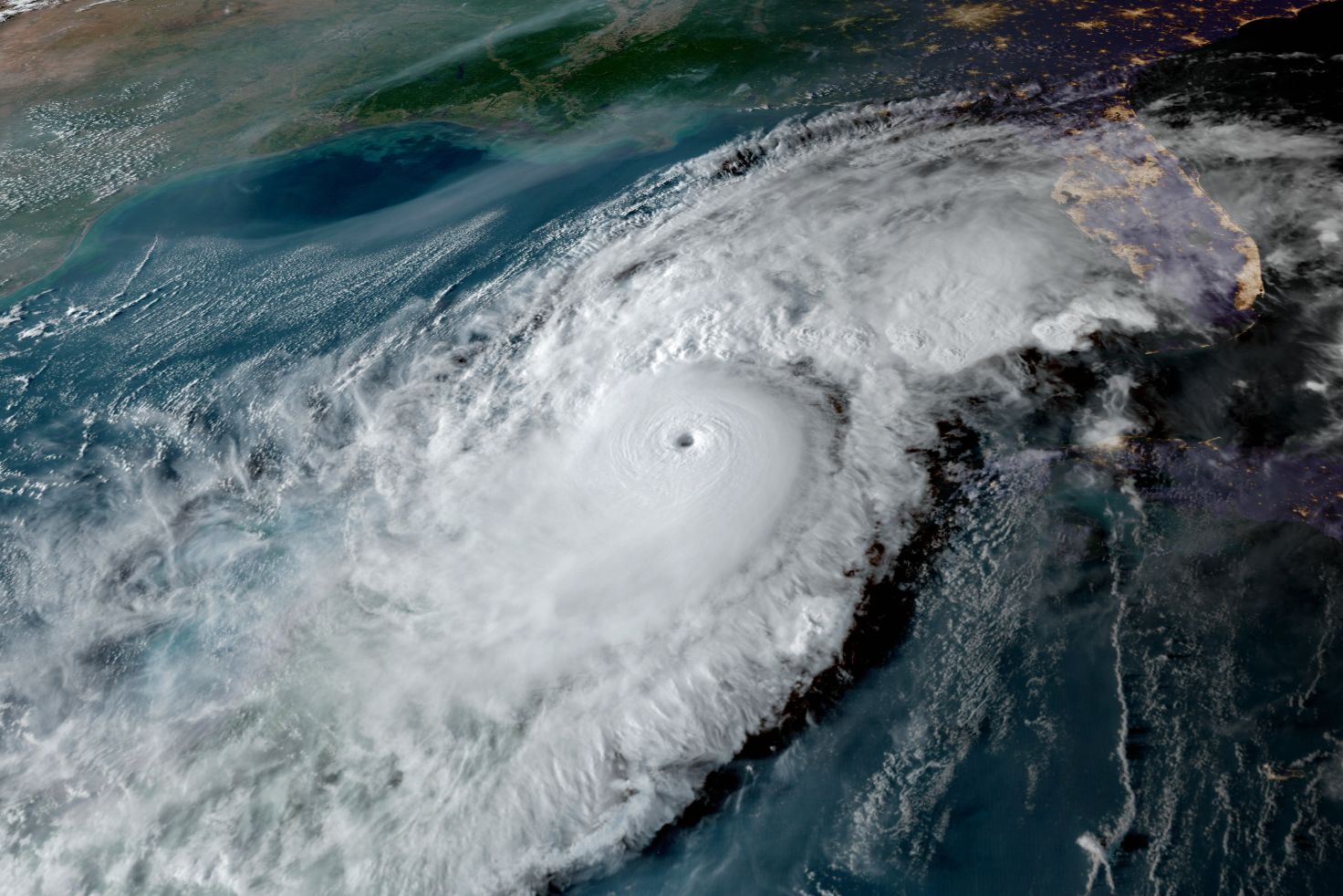

Hurricane Ian caused widespread damage throughout Southwest Florida.

Even before Hurricane Ian blasted ashore in September, my home insurance was set to spike by 40 percent this year. I don’t live in a flood zone and I have bare-bones coverage. What is going on? It’s a question many homeowners across the state are asking, and the issue is even more pressing in the wake of Ian, which caused an estimated $67 billion in insured losses, making it the costliest storm in Florida history.

Nationwide, home insurance costs roughly $1,600 on average each year. But Florida has the priciest policies in the nation, with some areas more than tripling that. In Miami-Dade County, it’s $5,093 a year, rising to $6,729 in the Florida Keys. In Sarasota County, our average rate is roughly 35 percent more than the national average, at $2,470. And the numbers are going up.

“Over the last year, I’ve seen 10 to 50 percent rate increases. Last year, one company had a 111 percent increase,” says Paul Jorgensen, a local agent with Florida Farm Bureau Insurance. Tanis Perez, executive vice president for the southeast for Premier Concierge Insurance, has seen a similar trend, with the price of some policies doubling overnight.

According to Jorgensen, rates were climbing before Ian in part because of the increased cost of building supplies and labor, but he says that’s negligible in the face of other factors, like the decreasing number of insurance providers willing to do business in Florida. Six companies have recently gone insolvent, and others are not renewing policies for next year.

“Altogether, it’s almost 10 fewer companies doing business in Florida in the last year—that’s a lot,” says Jorgensen. In July, state regulators placed 27 companies on a watch list because they were deemed financially unstable. Two significant culprits are litiga-tion costs and roof fraud.

“Florida is the most hurricane- and litigious-prone state in the country,” says state Sen. Jeff Brandes, a Republican from Pinellas County. “Other states had less than 1,000 homeowner’s insurance litigations last year. We had 107,000, even though there was no storm. As a result, the insurance industry lost $1 billion each of the last two years. Even before Ian, they were on the path to losing that amount this year.”

Nearly 80 percent of all homeowner’s insurance lawsuits nationwide are filed in Florida, which accounts for just 9 percent of all homeowner claims, according to the office of Gov. Ron DeSantis.

Why so many lawsuits? “Public adjusters and roofing companies team up with attorneys and offer free roof inspections and unassuming home-owners let them,” says Jorgensen. “They’ll find some damage and tell the homeowner, ‘We’ll take care of it,’ and ask for them to sign off on an assignment of benefits agreement to the roofer.” That signature effectively removes the homeowner from the equation. Communications from then on happen between the roofer and the insurance company.

“The insurance company then receives an inflated cost to repair the roof and if they refuse to pay it, it moves to litigation,” says Jorgensen. “So now the insurance company is paying attorneys, even though maybe the roof is just old. And if insurance companies have to replace everyone’s roofs and pay for litigation, everyone’s rates go up.”

Another factor contributing to the rise in costs is that insurance companies also purchase their own insurance, called reinsurance, to pay out claims after sweeping disasters like Ian. Just like consumer-facing insurance companies, some reinsurers are pulling out of the state, while others are raising rates by as much as 50 percent. As Florida homeowners repair damage caused by Ian, it will likely push many toward what industry insiders call the “insurance of last resort,” Citizens Property Insurance Corporation, a state-backed, tax-exempt company that often offers the cheapest, most lax coverage available to consumers.

Like private insurance companies, Citizens is funded by policyholder premiums. However, state law requires that Citizens levy assessments on Florida property insurance policyholders—meaning they have access to the premium pools of private insurance companies to draw on—if it experiences a deficit in the wake of a storm, potentially raising rates for everyone. As private insurers tighten requirements and increase their prices, Citizens is growing quickly, covering 1.1 million policyholders statewide—a number that jumped by 300,000 in just the past year. But Citizens insists it can shoulder the growth.

“Citizens is in a strong financial position and will be able to pay claims from Hurricane Ian and still have reserves left over for the next storm,” says Michael Peltier, a spokesperson for the company. But as the number of Citizens customers rises, so does the company’s exposure and so does the possibility of rates going up for all Floridians. “That is the risk,” says Peltier.

In May, state lawmakers passed a bill addressing roof fraud. Championed by state Sen. Jim Boyd, a Republican from Manatee County, the law created a $2 billion reinsurance fund to help insurers pay potential hurricane damage claims, put new limits on insurance lawsuits and attorney fees, circumvented the lure of roof companies by offering hurricane mitigation inspections and allowed policies with separate deductibles for roof damage, which will leave some homeowners shouldering more of the cost of roof replacements.

“Insurance companies are prepared for these storms,” says Boyd, “but are not prepared for fraudulent claims that drove costs up dramatically.” He believes the changes will lead to reduced rates for consumers. Although the bill passed with bipartisan support, Democrats say the move falls short and fails to grant immediate financial relief to homeowners with ballooning premiums. Republicans acknowledged it will take 12 to 18 months before prices may drop.

Add the homeowner’s insurance crisis to Sarasota’s affordable housing crisis, and you’ve got a situation that makes homeownership a pipe dream for many.

“For now, I think this is going to hit your local homesteader hardest, the person who is trying to afford a home to live in,” says Jorgensen. “I’m talking about the people who check you out at Publix, fill your Starbucks in the morning and teach your kids.”